The joint interpretive guidance published by the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission in the Federal Register on March 18, 2026 marked a clear attempt to replace years of fragmented crypto oversight with a more structured classification system. By setting out five formal categories for digital assets, the agencies gave the market a framework that many participants had long argued was missing under the prior enforcement-driven approach.

The immediate significance of the guidance lies in its boundaries. The new taxonomy narrows the set of digital assets likely to be treated as federal securities and outlines explicit conditions under which a token can stop being viewed as an investment contract. That change does not eliminate legal uncertainty, but it does give firms a more usable foundation for custody, listing, disclosure and compliance decisions.

the SEC guidance from tuesday on what constitutes a security (and what does not) puts a final nail in the gensler era’s coffin

but while it gives supportive clarity for at least the next 30 months, the CLARITY Act could provide a durable legal foundation for the next 30 years 💡 https://t.co/86M6ewgyvF

— Alex Thorn (@intangiblecoins) March 20, 2026

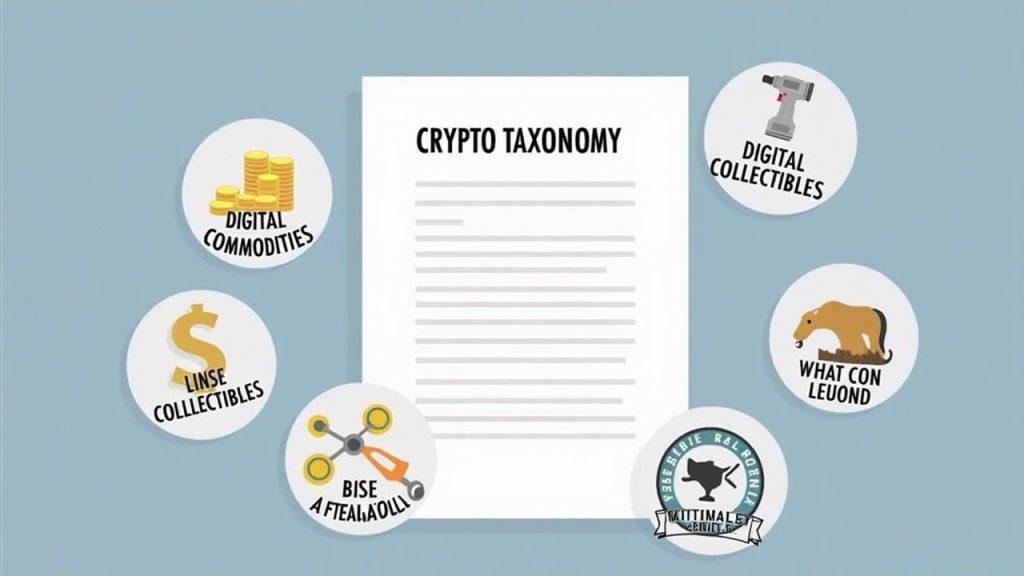

A Formal Taxonomy Replaces a Looser Enforcement Model

The guidance divides digital assets into five categories and links each to a more defined regulatory treatment. Digital commodities are described as assets primarily used as a store of value or means of exchange and generally overseen by the CFTC. That category reflects the agencies’ effort to distinguish market-driven crypto assets from instruments tied to capital-raising or issuer dependence.

The framework also separates out other token types with more precision. Digital collectibles are treated as unique tokens whose value comes mainly from scarcity or cultural significance, digital tools are tokens used for access or functionality, stablecoins are pegged tokens meant for payments or stability, and digital securities remain the assets that still fit within securities law under a narrower Howey analysis. By defining those categories directly, the agencies signaled that not every crypto asset should be evaluated through the same regulatory lens.

Just as important as the categories themselves is the lifecycle test built into the interpretation. The agencies said a token issued during a fundraising phase may later stop being treated as a security if governance obligations are completed, decentralization is achieved, the project is abandoned or the issuer becomes inactive. That off-ramp is one of the most consequential parts of the guidance because it introduces a formal way for a token’s legal character to change over time.

The Guidance Offers Clarity, but Not Finality

The agencies also clarified that certain common crypto activities will generally not be treated as securities transactions. Airdrops, mining and staking were all identified as activities that typically fall outside the securities framework under the new interpretation. That point matters because it reduces pressure on some of the operational behaviors that had remained clouded by years of broader enforcement theories.

Industry reaction reflected how sharply the guidance contrasts with the prior SEC posture. Market analysts described the interpretation as a meaningful break from the expansive reading of the Howey Test that had defined the previous era of crypto regulation. Alex Thorn of Galaxy Digital called it the “final nail” in that earlier approach, while SEC Chair Paul Atkins said on March 19, 2026 that the agency was moving away from what he described as a persistent failure to provide clarity.

Still, the guidance is interpretive rather than legislative. Its practical effect is immediate, but its long-term durability still depends on Congress. That is why the CLARITY Act remains central to the broader policy picture: lawmakers still need to codify market-structure rules, and that effort continues to face disagreements over stablecoin yield, open-source developer protections and DeFi-related provisions.

The next step is operational rather than theoretical. Trading eligibility, custody policies, token review procedures and governance disclosures all need to be updated to reflect the new taxonomy and the reclassification pathways set out in the guidance. The agencies have drawn clearer lines, but companies will still need to prepare for further legislative changes that could reshape the final rulebook.