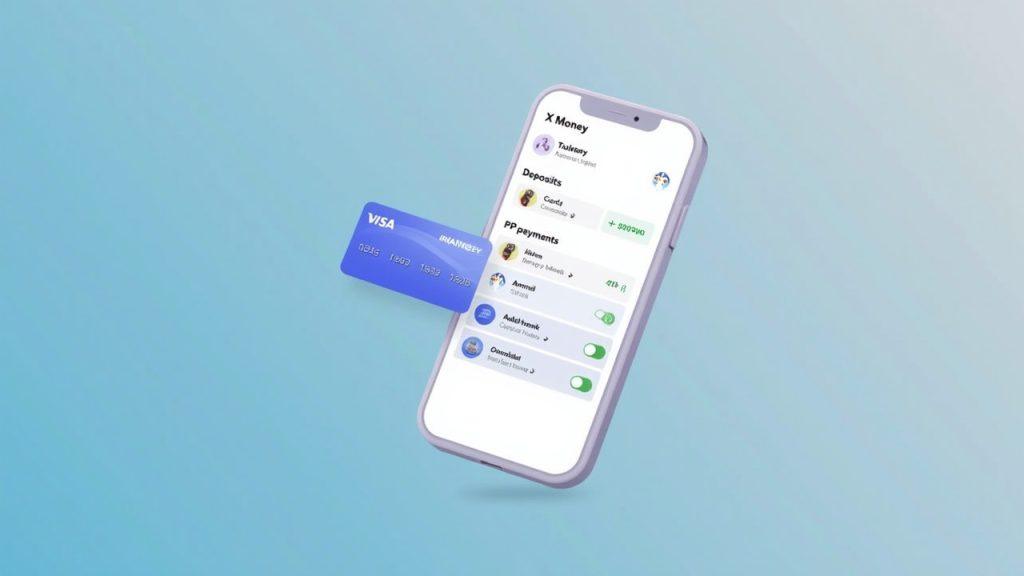

X began showing the first images and limited beta access for X Money in early March 2026, revealing a wallet-style product that supports deposits, person-to-person transfers, and an advertised yield feature tied to Direct Deposit. This is X putting a financial layer inside the social platform—less “payments as a feature” and more “payments as a product line.” The immediate consequence is that compliance and operational accountability moves from theoretical to executable: if you’re offering deposits, transfers, and yield messaging, regulators and partners will expect bank-grade discipline around controls, disclosures, and customer outcomes.

What the beta surfaced is fairly clear: send money, receive deposits, and a headline yield of up to 6% APY via Direct Deposit. X is positioning X Money as a broad platform wallet—supporting P2P, merchant payments, creator monetization, and card functionality—not as a crypto exchange. That distinction matters because it affects which regulatory buckets the product falls into and which obligations “attach” to the operator.

Here’s a few more screenshots. There’s a debit card with cash back too! 😳😱 pic.twitter.com/yeKE1gXAjQ

— William Shatner (@WilliamShatner) March 3, 2026

Where X is drawing the line and why it matters

On February 14, 2026, X’s Head of Product, Nikita Bier, drew a bright boundary: “X is not handling trade execution or acting as a crypto brokerage. Just building the financial data tools and links.” That statement is operationally important because it frames X as a payments and wallet operator rather than a broker-dealer or crypto exchange. In compliance terms, it pushes trade execution, custody, and market-conduct responsibilities away from X and toward licensed intermediaries if crypto rails ever appear later.

This is the right way to interpret the current footprint: X Money looks like a regulated money-movement and wallet product, not a trading venue. That classification informs everything from KYC/AML design to disclosures, dispute processes, and record retention.

The licensing and partner infrastructure behind the beta

X has described meaningful groundwork on the regulatory side, including money-transmitter licences in more than 40 U.S. states. Those licences anchor the product inside state-level supervisory frameworks and are typically paired with expectations around consumer protection, AML program design, complaint handling, and periodic examinations.

X has also emphasized partnerships with card networks and payment firms, including a previously announced collaboration with Visa in January 2025. Those relationships matter because they define settlement dependencies, chargeback and dispute mechanics, and where certain compliance controls actually live. In practice, a wallet product is only as stable as its banking and network counterparties, especially when it’s promising a yield feature that draws user attention and can be interpreted as a deposit-like benefit.

The crypto speculation problem: reputational risk versus product reality

Public chatter about crypto support has been persistent—Dogecoin comes up often due to Elon Musk’s history, and XRP and Bitcoin have also been pulled into speculation tied to partners and old narratives. Reports have pointed to Cross River Bank’s historical use of Ripple’s protocol since 2014 as a reason XRP keeps showing up in conjecture. But based on the product leadership’s own statement, token support remains speculative until X publishes real technical and compliance specs.

This is where the risk becomes a communications and conduct issue. When senior accounts amplify predictions or repost speculation, it can create expectations that outpace what the product is licensed and architected to do. For a payments product, that gap can trigger supervisory questions, partner-bank discomfort, and avoidable reputational exposure.

As the beta expands, the decisive factor will be the technical architecture and counterparty arrangements X eventually publishes. Until those are released, the defensible baseline is what X has already stated: a wallet and payments layer with state licensing and partner-bank dependencies, not a crypto brokerage.